What Is a Payment Gateway?

A payment gateway acts as the bridge between the checkout page and the financial institutions involved in a transaction. It securely transfers payment information so the processor and bank can confirm whether the charge is approved.

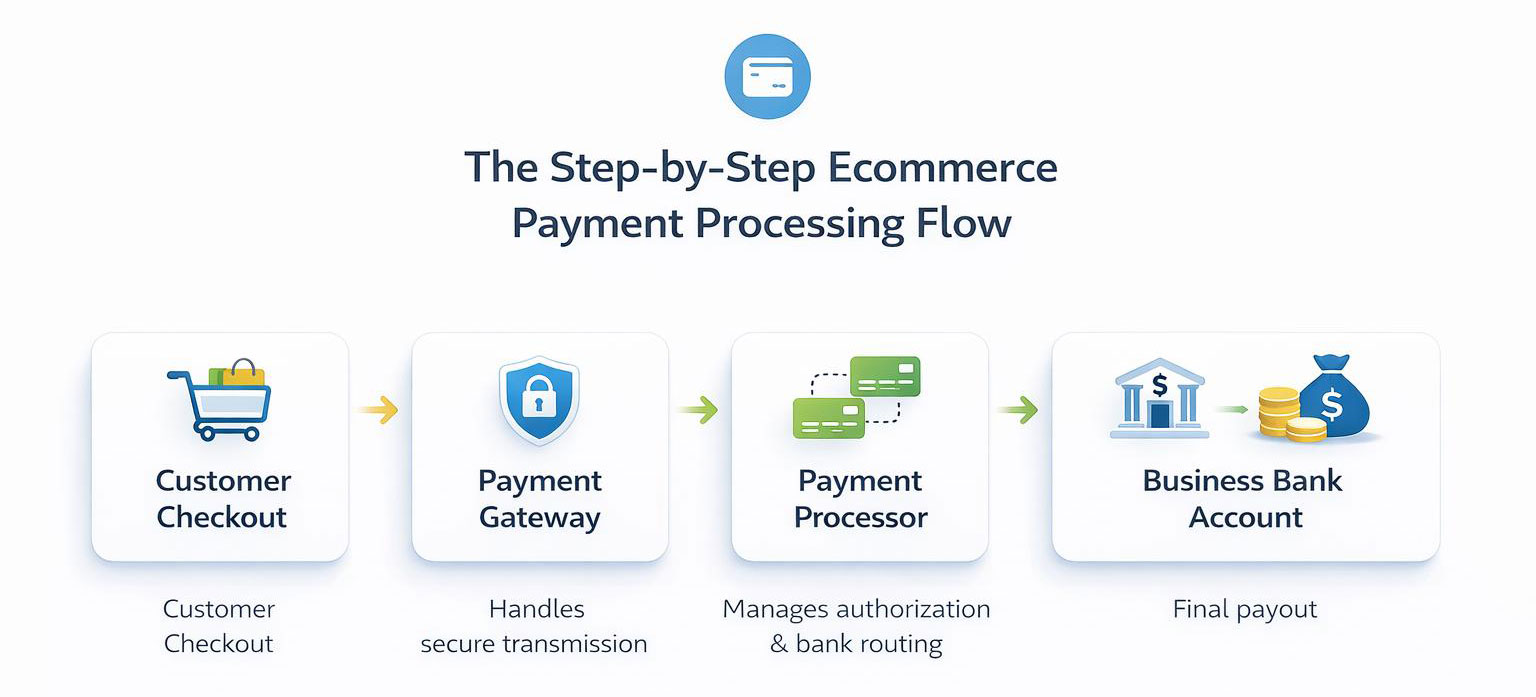

What a Payment Gateway Does During Checkout?

During checkout, a payment gateway handles the secure approval of an online payment. It works in the background to verify the transaction before an order is confirmed.

Behind every successful checkout:

- Payment details are securely captured.

- Data is encrypted to protect customer information.

- The authorization request is sent to the processor and bank.

- A real-time approval or decline is issued.

- The result is instantly displayed to confirm the purchase.

A payment gateway does not move funds or settle payments. It only facilitates authorization so the transaction can proceed securely.

Why Payment Gateways Exist?

When customers shop online, they share private payment details. That creates risk if the data is not handled properly. Payment gateways exist to provide that secure communication layer.

They:

- Securely pass payment information to the bank

- Shield card data from being exposed

- Flag potentially risky transactions

- Make sure payments are approved before orders go through

- Give ecommerce stores a safe way to accept digital payments

What Is the Difference Between a Payment Gateway, Payment Processor, and Merchant Account?

A payment gateway, payment processor, and merchant account serve different purposes in an online payment system:

- The payment gateway securely transmits payment data.

- The payment processor connects with the issuing and acquiring banks to handle authorization.

- The merchant account holds funds before payout to the business.

They operate together but handle different responsibilities within the transaction lifecycle.

Where Payment Gateways Fit in the Ecommerce Journey?

Every ecommerce purchase follows a sequence: browse, add to cart, review, and checkout. After a customer clicks “Pay,” the payment gateway quietly checks the transaction. Only when it’s verified, order gets confirmed.

This is where it shows up in the buying process:

- At checkout – It steps in right after the customer clicks “Pay.”

- Before order confirmation – It confirms the payment before the store finalizes the order.

- Invisible during smooth transactions – When everything works, no one notices it.

- Critical for payment trust – Its security is what makes customers feel safe completing the purchase.

- Most visible when something goes wrong – It usually only gets attention when a payment fails or slows down.

The gateway is not part of browsing or cart selection. It exists solely to secure and verify payment at checkout.

What a Payment Gateway Is — and Is Not?

Payment gateways are often confused with other payment components. The table below clarifies what a payment gateway does — and what it does not do.

What Payment Gateway Does |

|

|---|---|

| A Payment Gateway Is | A Payment Gateway Is Not |

| A secure transaction facilitator between checkout and the banking network | A bank |

| Required for online card payments | A digital wallet that stores customer money |

| Responsible for encrypting and transmitting payment data | The visual checkout page customers interact with |

How Payment Gateways Affect Conversions and Trust?

Payment gateways operate quietly — but their influence on revenue is significant. A smooth, secure transaction experience directly impacts whether customers complete their purchase.

Its impact includes:

- Improved payment reliability → Every successful transaction preserves conversion value.

- High-speed authorization → Measurable lift in checkout performance.

- Confidence-driven processing → Customers feel secure when systems feel familiar.

- Minimal friction → Any delay or decline increases the risk of abandonment.

Behind every successful checkout is a gateway that works flawlessly.

What Are Common Payment Gateway Issues?

Even reliable systems are not immune to friction — especially at the final step of payment authorization.

Typical performance gaps include:

- Transaction declines that provide little or no explanation to the customer

- Authorization delays that disrupt checkout momentum

- Limited payment method availability

- Cross-border processing inconsistencies

- Suboptimal performance on mobile devices

When these issues occur, shoppers often lose trust in the brand— even when the problem stems from the platform, not the store itself. If that sounds familiar, migrating to Shopify removes most of these friction points before they start.